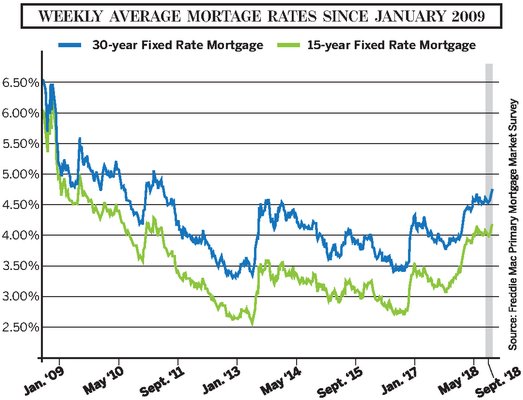

The scope of fluctuating 30- and 15-year mortgage rates over the past decade. According to Freddie Mac, recent mortgage rates have bounced between 4 percent and 4.7 percent, which is high compare to a year ago but way lower than the rates a decade ago. The lowest rates seen in 10 years were around April 2013 at 3.4 and 2.6 percent, respectively. MICHAEL PINTAURO

Mortgage rates in the 30-year and 15-year fixed-rate terms have hit new seven-year highs, around the 4.7 percent and 4.2 percent marks, respectively, according to data from mortgage buyer Freddie Mac.

Rates are roughly 1 percentage point higher than this time one year ago—but historically low in comparison to the double-digit highs of the 1980s. The Federal Reserve raised its benchmark interest rate a quarter-point to 2.25 percent in September—it’s third hike this year—signaling that the cost to borrow will only rise for the near future.

John F. Wines, a licensed associate real estate broker at Saunders & Associates in Southampton, said the second-home market may be affected eventually, but it is buyers on the lower end who are most impacted by rising mortgage interest rates.

“There is a difference between a primary residence and a vacation, second home. If interest rates continue to go up on a regular basis, it does affect the disposable income to be able to buy a second home,” Mr. Wines said. “The requirements are going to get harder and harder to buy a home out here. There are financial milestones that are required to get a mortgage on a second home, compared to a first home. It could potentially affect sales, especially on the lower end because they don’t have the disposable income. How much can they qualify for?”

The market has largely recovered from when the housing bubble popped in 2008, when more than 30 percent of homeowners owed mortgage lenders more than half the value of their homes. According to a May study by the home search and data company Zillow Group, more than 4.4 million Americans have mortgage debt that exceeds the value of their home and remain underwater on their mortgage payments and hold onto their homes instead of selling for a loss.

“In corners of the country where home values have been stagnant in recent years, recent homebuyers can easily fall underwater, particularly those who buy with small down payments,” Zillow senior economist Aaron Terrazas said.

“For the past few years, historically low mortgage rates provided the silver lining for buyers as prices rose higher and higher,” Mr. Terrazas said, but that may be a relic of the past. Zillow found mortgage payments growing less affordable in a separate study released in June.

Homeowners who are underwater on their mortgages, or who are just struggling to keep up with high monthly payments, can refinance. According to the first quarter report of The Federal Housing Finance Agency—which regulates Fannie Mae, Freddie Mac and 11 federal home loan banks—more than 73,800 homeowners nationwide could still borrow through the federally sponsored Home Affordable Refinance Program this year. However, the program is set to expire at the end of December after it was extended twice since 2016. To qualify for the federal refinance program, a homeowner must have a remaining balance of $50,000 or more on their remaining 10 years of mortgage payments with rates 1.5 percent higher than current market rates.

There are many more options for homeowners who are not in a dire situation but want to take advantage of lower mortgage rates offered by private banks.

But as for when is the best time to take the plunge on refinancing, Christine Curiale, the vice president sales manager of Valley National Bank-Residential Mortgage Southampton branch, said refinancing should always be strategic.

“It is strictly a numbers game. They either make sense for your overall financial goals or do not,” Ms. Curiale said. “Overall cost, interest rate and term all play a factor in your strategic planning. … Take the time to review all options based on your overall financial goals.”

There are many scenarios in which to consider refinancing. Ms. Curiale said that if residents have a goal to keep their home and get out of an adjustable rate mortage, she’ll suggest a more secure, fixed rate. For residents looking to pay off their mortgage faster and build equity at the same time, a policy with a fixed rate and bi-weekly payments can speed things along.

“On the flip side, if your goal is to have the mortgage paid off in five, seven or 10 years and you have a definite plan in place to do so,” she said, “some may consider taking advantage of a lower, adjustable rate mortgage to save money within that term.”

After reflecting on decades working for Saunders, Mr. Wines recalled a disproportionate number of luxury-home buyers make all-cash deals without any mortgage financing. “They drop the cash on the table, with no mortgage, and the deal is done,” he said.

These type of deals happen every year, and just blow Mr. Wines out of the water. But when second-home buyers do opt to mortgage their homes, it’s for financial planning purposes and not out of necessity, Mr. Wines said. He noted these buyers want to use their disposable income to play with other investments, instead of burying it in real estate. “They can get a mortgage loan at 4 percent but they are earning 6, or 8, or 15 percent elsewhere. So, they borrow the money at cheap rates and keep their free capital investments in whatever investments they have, either the stock market, hedge funds or other investment vehicles.”

And on the selling side, it can be advantageous not to have to deal with a mortgage. Mr. Wines said sellers may be more willing to make a deal if there isn’t a mortgage contingency.

“From a seller’s point of view, they are happy to have a contract without a mortgage contingency because they know if the buyer puts 10 percent down and the deal doesn’t close, they get to keep the deposit. With a mortgage contingency clause, the seller has to return the deposit if the deal doesn’t go through,” Mr. Wines said.

Rates, overall costs, tax deductibility and timing play a factor in deciding to purchase a large financial asset—Ms. Curiale said this is particularly true of the second-home buyer.

“In fact, many of them are now considering alternative ways to leverage down payment money since some financial advisers are guiding their clients to stay in the market versus cashing out to buy a vacation home. If their money is working for them in their current investments they are less likely to pull it out,” she said.

Ms. Curiale pointed to Unison funds—a down payment partner made up of university endowment funds and pension funds where a buyer can put down as little as 5 percent into the home and Unison can make up the remainder of the 20 percent minimum down payment in exchange for a percentage of the appreciation—as a way to keep buyers’ investments working for them while they purchase a home at the same time.

“For many, this new and innovative program allows people to leverage and capitalize on the housing market while limiting their cash outlay,” she added.

Another way second-home buyers might have already found a way to game a mortgage is to purchase a property through a limited liability company as a rental investment, said Dana Trotter, a Sotheby’s International Realty senior global real estate adviser and associate broker.

“One strategy we’ve seen to take advantage of a mortgage-interest deduction on a second home is to purchase the property with an LLC and then rent it out when not in use. By setting it up as a rental investment property, the owner can deduct the mortgage interest, collect rent to help with carrying costs, and still enjoy the property at their leisure. We would, of course, advise anyone planning to do that to work closely with their tax adviser to make sure it is done properly,” Ms. Trotter said.

on Oct 1, 2018

on Oct 1, 2018