COURTESY DOUGLAS ELLIMAN

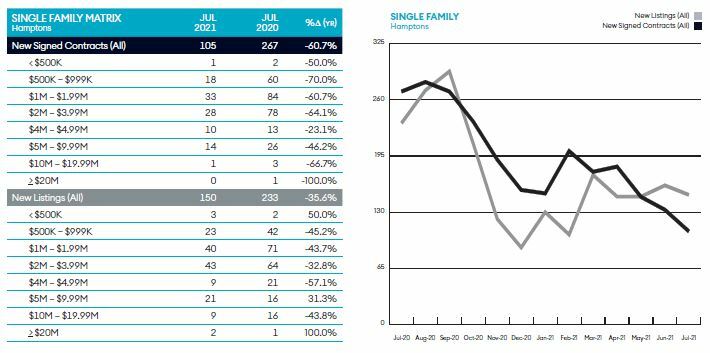

The number of new signed contracts for Hamptons single-family homes was 105 in July, according to The Elliman Report, a 60.7 percent decline compared to the same month last year, but market watcher Jonathan Miller warns not to get the wrong impression.

Mr. Miller, the president and CEO of Miller Samuel Inc., a real estate appraisal and consulting firm, says the decline in the number of deals inked is not a sign of market weakness. Rather, it reflects just how low the supply of homes for sale is in the Hamptons right now — listing inventory fell 43.3 percent mid-year to 1,081, the third-lowest level in nearly 15 years.

The other important factor to consider is that July 2020 saw the release of pent-up demand that built during the pandemic lockdown in New York State. A repeat of that level of activity could not be expected.

“Clearly, the Hamptons for the last year has been an odyssey in the sense that seasonal patterns weren’t followed,” Mr. Miller said during a recent interview. “The release of pent-up demand, combined with record-low and falling mortgage rates, and a rethinking of remote working, laid havoc on the Hamptons market. The demand, as a tsunami, significantly overpowered the inventory that was available.”

The Hamptons market is cooling now, even as Manhattan is booming, he said, but he attributed that cooling to a lack of supply more than anything else: There are simply not enough homes for sale to satisfy the buyers.

The “months of supply” shows that the pace of the market was incredibly swift in the second quarter of the year. “The number of months it would take to sell all inventory at the current rate of sales was the lowest — meaning the fastest — on record at 4.8 months,” Mr. Miller said. “The market was literally 63.6 percent faster in the second quarter than it was in the same quarter last year.”

The number of days that a house spends on the market between its listing date and its closing date fell 31 percent in the second quarter to 109, while the discount off the last asking price slipped from 13.1 percent to just 6.3 percent. Roughly one out of five homes sold in the Hamptons went for even more than the asking price was.

Mr. Miller said the feast and famine pattern in the Hamptons for the last year and half since the pandemic began has been exhausting.

“We’re also seeing record pricing,” he went on to say. “The Hamptons market for median and average sale price were the highest we’ve ever tracked. Median was $1,405,000, and the average was $2,416,000.”

The share of homes sold for less than $1 million was 45 percent, a record low since Mr. Miller began tracking the figure in 2011.

It’s quite astounding, and no one who follows this market could have expected this trajectory, he said, adding that the same can be said about virtually every housing market. “The Hamptons is no different than what we’re seeing across the U.S.,” he said. “… It’s a very similar narrative: record prices, heavy sales volume and unusually low inventory.”

He advised to not assume that when the market is rising that it will rise forever, just like no one should assume a falling market will fall forever. “The market is not linear,” he said. But he also sees signs that the housing market has some good years ahead of it.

The billions if not trillions of dollars of economic stimulus coming through over the next several years fuels a robust economic environment, which in turn stimulates housing demand, he said.

The current market is not a housing bubble like the one seen in 2007, when all a borrower had to do to receive financing was fog a mirror, he said. “Mortgage underwriting at lenders is much tighter than historical norms.”

Back then, “it was a global thermonuclear credit bubble that broke down,” he said, and housing was a symptom, while today when people can’t afford the prices anymore, the prices level off. “Imagine that,” he said. “That’s actual pure supply and demand forces at work.”

Nationwide, the percentage of household income that goes toward debt service is half of what it was during the bubble, he pointed out. The worst case scenario, he said, is that the overwhelming demand will level off — there will be a plateauing as opposed to a correction.

“I’m uncomfortably optimistic,” Mr. Miller said. “I am having a hard time finding significant future weakness in the picture.”

He added that he is not forecasting a boom, but the economic stimulus, the interest rates locked at lower levels and the eventual control of the pandemic lead him to believe there is still upside ahead.

One open question is the future of remote work and what that will mean for the second-home markets like the Hamptons that have benefited from it. There are “years of exploration ahead” before the answer is known, according to Mr. Miller. “How that plays out, it still hasn’t been firmed up.”