Streptocarpus COURTESY WILDFEUER RETURN TO MONTAUK / RÜCKKEHR NACH MONTAUK

Even today, costs related to property damage from high-velocity winds and flooding during Superstorm Sandy are still being felt.

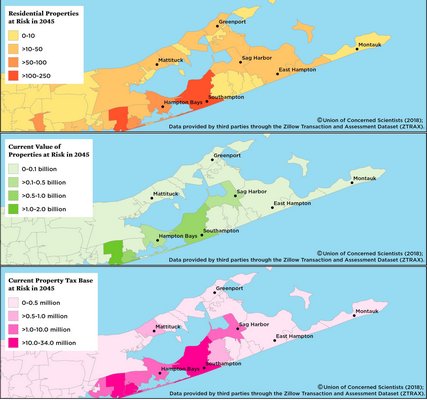

Though many South Fork homeowners and municipalities have taken measures to mitigate wind and flood damage in the nearly six years since the devastating hurricane struck Long Island, a study by the Union of Concerned Scientists that was released last month shows that flooding on the East End is only expected to get worse. The study documented the potential impact of rising sea levels and flooding on property tax revenue among at-risk municipalities—Southampton landed at the top of the list, second only to Southern California.

“It’s flooding that happens during high tide, and it doesn’t require a storm—but is absolutely worsened by one,” said Kristina Dahl, Ph.D., a senior climate scientist at the nonprofit science advocacy organization. Dr. Dahl was one of the authors of the study, which attributes rising sea level to climate change.

Dr. Dahl said storm surges build up water off the coast that makes landfall, slushing the ground. She said nuisance flooding is something Long Islanders, especially those on the South Fork, should be wary of.

The study was released as homeowners continue to weigh the options for protecting their homes from future storms—because storms are undoubtedly coming, according to the National Oceanic and Atmospheric Administration.

NOAA has forecast a near- or above-normal hurricane season in 2018. That was also the case last year, when a tropical storm that was an offshoot of Hurricane Jose in September brought heavy rain and 20- to 30-mph winds, with gusts up to 45 mph, as well as flooding in low-lying areas on the South Fork. Other storms like Hurricanes Harvey and Maria devastated communities in Texas and Puerto Rico, but lost momentum before reaching the Northeast.

In the aftermath of storms, property owners largely have relied on flood insurance—which is mostly sold through the National Flood Insurance Agency, although there are a few private insurers out there—to protect their homes. The problem is the federal program may lapse: Congress’s deadline to renew the program is midnight on July 31.

The flood program is expected to be able to pay $5.5 billion in claims this year, which would be available for homeowners with existing policies, according to FEMA. But a lapse would limit the federal program’s ability to seek additional funds through borrowing.

A lapse is “unlikely,” according to a notice on FEMA’s website, adding, “FEMA and Congress have never failed to honor the flood insurance contracting in place.”

Nevertheless, due to either storm surges or rising sea levels—about 1 foot by 2030—Southampton is positioned to have millions of dollars of property tax revenue at risk due to the amount of chronic flooding expected on the East Coast—about 26 times per year.

According to the report, 227 homes, with a total value of $1.4 billion, are at risk in Southampton. At that valuation, $27 million in property tax revenue is at risk, or 0.6 percent of the total property tax revenue. East Hampton Town’s at-risk property is considerably lower, at $392,000, impacting only $7,600 of the tax base.

Luxury home value and population size are factors that drive up the property tax revenue at risk, Dr. Dahl said, which is why East Hampton is not higher on the list.

“Exposure is highest where topography is lowest and where populations are more dense. We are looking at fewer homes exposed, because there are fewer homes there to begin with. But it could be also the elevation of the land,” Dr. Dahl said.

She noted that East Hampton is surrounded by water, so it’s a “no-brainer” for officials to pay attention to flood mitigation as well.

“While property values could be affected negatively by this kind of chronic flooding, the loss of property tax revenue to the community could also have a big impact,” Dr. Dahl said. “Property taxes fund our schools, they fund our transportation systems, they fund our upgrades that we often vote for so that we can improve flood mitigation. In a place like the Hamptons, where you have a lot of tourism as well, having less in tax money coming in could negatively impact the economy.”

In general, flood insurance premiums rise to better reflect the actual risk properties face in the next decade. Some homeowners may be able to afford that insurance on the South Fork, while others may not.

“The wealthier homeowners will hold on to their properties despite the growing cost of flood insurance. But you can also imagine a situation in which properties are flooding frequently enough that insurers say, ‘This isn’t worth the risk anymore,’ having to pay out over and over, and flood insurance suddenly becomes unavailable,” Dr. Dahl said.

“Even a wealthy homeowner doesn’t want to see their home flooding repeatedly. Even if they can afford to bail it out—is that really a place you want to be living? And the average person will be disproportionately affected, as they have more money tied up in their property.”

East Hampton’s Coastal Assessment Resiliency Plan, which was released in May 2017, and the New York State Department of Environmental Conservation’s analysis both depict similar outlooks by 2030: the Atlantic Ocean will rise an average of 1 foot off the coast of Montauk by 2030. Unlike the Union of Concerned Scientists numbers, FEMA has outlined Napeague, downtown Montauk, Lake Montauk North, and Northwest Harbor, as well as East Hampton Village and Wainscott, as in “extreme risk” of coastal flooding.

The estimated market value at risk is somewhere between $249 million and $493 million north of Montauk Highway, $1.5 billion south of the highway, and $2.1 billion in Napeague.

Samuel Merrill, the project manager of East Hampton’s resiliency plan, has said strategies to prevent damage include investing in and reinforcing public infrastructure and seawalls, as well as floodproofing homes.

According to Southampton’s Coastal Resources & Water Protection Plan in 2016, the town is a participating member in the National Flood Insurance Program to aid residential and business property owners and renters as long as they follow standards for development detailed in the town code. Property owners are also “generally required to purchase flood insurance if there is a mortgage from a federally regulated bank,” of which the maximum insurance coverage is $250,000 for a residential structure. The cost of flood insurance in both communities is reduced by adopting flood management measures that exceed the federal program’s requirements.

Again, with the flood insurance program in limbo, the extent of the coverage for residential properties—especially new builds—is up in the air.

As far as private insurers go, hundreds of homeowners on the East End use AIG, which recommends proactive measures to protect against floods in addition to flood insurance.

“As far as the renewal of the flood insurance program, we have been here before. It’s a political football. I hope that cooler heads prevail because it’s an important piece in most people’s financial insurance plan to have flood insurance as part of their protection plan,” said Steve Poux, AIG’s head of global risk management.

He said it is better for a homeowner to avoid a loss, than it is to file a claim and deal with the disruption that comes with being out of their homes while repairs are being facilitated. “The more steps that are taken proactively will reduce that likelihood.”

In addition to helping clients create a crisis plan through AIG’s Hurricane Protection Unit, the insurer’s Private Client Group launched a program called Smart Build two years ago that connects AIG experts with builders, architects and contractors before and during construction to recommend design and structural features that mitigate future flooding. The average project budget is about $13 million for a new development.

“The premise of the program is to get a seat at the table while the plans are being formulated for a new house. That way, you have the maximum opportunity to impact what the final version of the constructed home will look like and how resilient it will be,” Mr. Poux said.

AIG and other private insurers deploy the latest tools of the floodproofing trade including additional freeboard—building several feet above flood level with additional poured concrete or cinder blocks—and Smart Vent—a flood vent that allows the flow of air and water through a crawl space so that the pressure outside of the home’s foundation does not exceed the interior, causing foundation walls to collapse. Smart Vent can be retrofitted into pre-existing homes, which have inferior ventilation that often clog during flood episodes. Multiple flood vents ganged together can provide protection for a large lower level.

There are also “dry floodproofing plans,” which entail the deployment of portable, lightweight, 4- to 6-foot-high barriers that can be installed around the perimeter of the property to keep water out.

JD Allen on Jul 9, 2018

JD Allen on Jul 9, 2018