COURTESY THE ELLIMAN REPORT

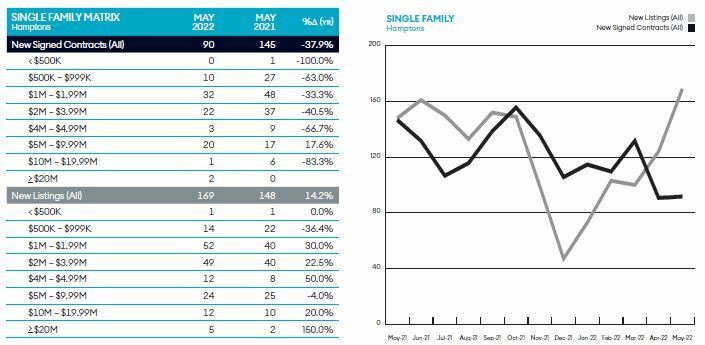

The number of single-family homes on the South Fork that entered contract in May was down by 38 percent compared to the same month a year earlier, a decline largely attributed to a dearth of houses for sale but also due to rising mortgage rates, according to The Elliman Report.

Newly signed contracts for single-family homes and condos combined have fallen each month, on a year-over-year basis, for 13 months, as sales fell from the pandemic highs. Even as the number of sales declined, inventory remained incredibly tight as there weren’t enough homes being put on the market to satiate the demand. However, last month was the first time in a year that the number of new listings added to the Hamptons market increased on an annual basis, rising 14.2 percent to 169.

Though new single-family listings overall are up, new listings for less than $1 million are down. While 23 listings below that threshold were added in May 2021, only 15 were added in May 2022, a 35 percent decline. At $1 million, and above, there were 125 new listings in May 2021 and 154 in May 2022, a 23 percent increase.

Above $10 million, there were 12 new listings in May last year and 17 new listings in May this year, a 42 percent increase.

The Hamptons’ inventory woes pale in comparison to the North Fork, where just 64 new listings were added in May, a 7.2 percent decline on an annual basis. Still, new inventory was more than double the number of single-family sales: 25, a 32.4 percent decline.

In the Long Island market, exclusive of the Twin Forks, new signed contracts were down 10.2 percent. Breaking down the data, the only price point were there was growth in the number of inked deals was between $500,000 and $600,000, where contracts rose 13.6 percent.

Inventory growth was just about flat: 3,305 new listings were added in May, which was 0.7 percent more than the number of new listings during the same month a year prior.

Staff Writer on Jun 9, 2022

Staff Writer on Jun 9, 2022