The median sales price and number of sales for the Hamptons luxury market, i.e. the top 10 percent of sales, quarterly since 2011.

The median sales price and number of sales for the Hamptons market quarterly since 2011. MILLER SAMUEL

The Hamptons luxury real estate market got off to a good start this year, but just as the first quarter was coming to a close, things quickly changed. Mandatory social distancing measures were implemented in New York State, including the halt of in-person real estate showings.

The scope of COVID-19’s effect on the market won’t begin to show in the statistics until the second-quarter results are in, but there is no denying that business has slowed. However, deals that were in contract or in negotiation before social distancing began have continued to close, and industry leaders remain upbeat that homebuyers will return in force when restrictions are relaxed.

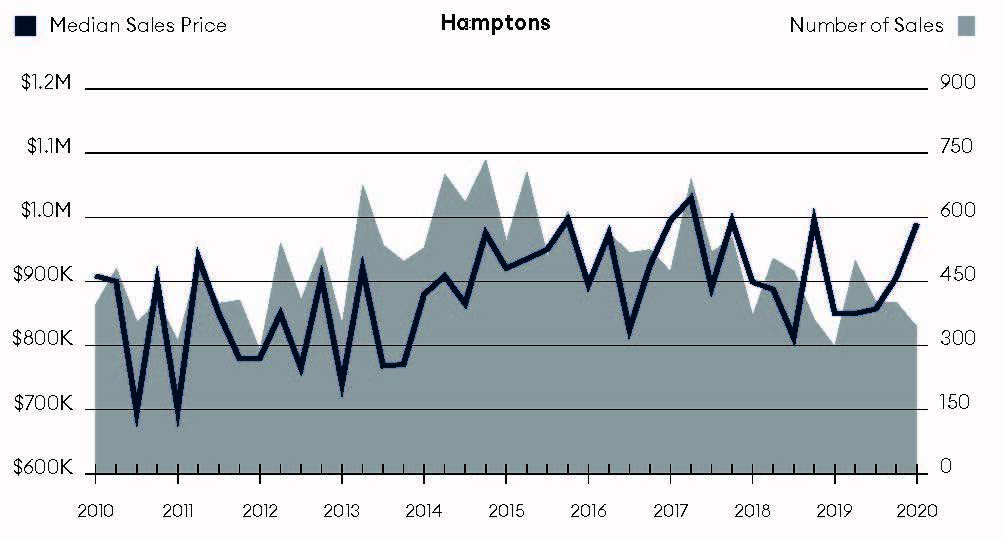

Total sales volume in terms of dollars was up, as were median and average prices, when comparing the first quarter of 2020 to the same quarter a year prior. According to the Elliman Report, the average sales price for a single-family home on the South Fork was up 26.3 percent, to $2.19 million, and the median rose 23.5 percent to $1.06 million. The point of entry for the luxury market — the highest 10 percent of sales — rose from $3.2 million to $4.01 million.

“We came into this first quarter very strong, as you can see,” said Todd Bourgard, Douglas Elliman’s senior regional manager of sales for the Hamptons. “It was an excellent, I would say, robust, first two and a half months. So we were looking at that thinking, ‘We’re really off to the races this year.’ And then this happened.”

But while COVID-19 concerns hampered the sales market, they had the opposite effect on rentals: A surge of New Yorkers looking to get out of the city began renting Hamptons homes for immediate occupancy in March and April, and interest in traditional summer season rentals from Memorial Day through Labor Day also spiked.

“The amount of people who came out here looking for rentals, sight unseen, was pretty incredible,” Mr. Bourgard said. “Of course, you don’t see that coming, and we all handled it very well: all the realtors, and all the brokerages.”

Looking back on rental contracts signed in December, January and February, 2020 started out as a strong rental year, and that has continued, according to Mr. Bourgard.

“There continues to be demand for Hamptons homes, so many tenants who normally would begin their rental on Memorial Day are here already,” said Ernie Cervi, Corcoran’s regional senior vice president for the East End. “Furthermore, some tenants have purchased the home they planned to rent — these are all good signs for a positive outlook for the remainder of 2020.”

The prohibition on house showings may not be a drag on the rental market, but for home sales, it’s another story. Virtual home tours are permitted under the state orders, but they don’t compare to visiting a home in person.

“There’s a big difference between a rental and a sale,” Mr. Bourgard said. “People can rent a home, and will rent a home, sight unseen by the photography that we have up and running on the internet. When you go to buy a home, it’s a very rare occasion that somebody will buy it sight unseen. They need to get in it, they need to feel it, they need to sit in it, they need to walk the property. It’s a whole different ballgame.”

Some homeowners are listing their houses now in anticipation of the state ban being lifted in mid-May, he said, but many are holding off until showings can resume.

“That ‘want to be out in the Hamptons’ exists,” Mr. Bourgard said. “So, I do believe, as soon as this ban is lifted, we’re going to see a lot of activity out here.”

He noted that, with few exceptions, every home sale that was already in contract went on to close. “The attorneys and title companies and appraisers have figured out ways to get this closed,” he said.

Robert Nelson, the executive managing director of the Hamptons for Brown Harris Stevens, also reported that sales that had been in contract, for the most part, closed successfully. That hasn’t been the case during many past economic downturns, he pointed out.

“If you go back and look at ’08-’09, and go back into periods of the ’90s, and go back to the period after the ’87 stock market crash, people walked from their deposit,” Mr. Nelson said.

In those cases, buyers knew the house they had planned to purchase lost more value than the amount of money they deposited on contract, he explained.

“Buyers are not walking from their closings, which means they perceive value is still there,” he said. “Otherwise, they would forgo their deposit and walk.”

When showings can resume, those who want to buy will have the money to do it, Mr. Nelson said. “This is a different period than it was in the ‘07-’08 phase, when people just truly didn’t have the money.”

Mortgages were involved in that financial crisis, he noted, and that’s not the case now. Credit is available now.

While phone calls are down at real estate offices, interest is up on the internet, according to Mr. Nelson. “This isn’t a time for our agents to be calling people asking what real estate needs they have, but we have seen a huge uptick in online views,” he said. “Will it translate to closings? We’ll have to see.”

He said he doesn’t like to make predictions, but his feeling is that the Hamptons market will be in a good position going forward.

The world has become familiar with working remotely and virtual meetings, he observed. “We’re never going to lose that.”

And that could bode well for Hamptons home sales.

Mr. Nelson said a reasonably sized house is more comfortable to work in than a much smaller apartment — even a three-bedroom Park Avenue apartment.

Real estate agents are also becoming accustomed to a virtual workplace, and Mr. Nelson expects it to stick.

“I don’t think we’ll ever lose that going forward. People are feeling very connected, in some cases more than they ever felt before in a large sense, a companywide sense,” he said.

Team meetings and regional meetings continue through video conferencing, and attendance is way up, he added, and local brokers are attending Q&As with Brown Harris Stevens President Hall Willkie and hearing from the top brokers in Palm Beach and Miami.

Mr. Bourgard reported that Douglas Elliman is having a similar experience: “We stay closer than ever before. Now you get everybody on a Zoom meeting. If Douglas Elliman has almost 400 agents out here, and we do a regional Zoom meeting, you’re going to have 80 percent of agents jumping on. There’s a real connection now.”